The great SaaS unbundling and why every CFO will have a larger, not smaller, tech budget

Why Your Tech Budget is growing as Software gets cheaper

Software is becoming radically cheaper to build, and your software bill is going to go up anyway. Remember the 2010s, when you were frustrated with high cable bills, internet charges, and cell phone overages? You asked yourself, “If I only watch sports, news, and the Food Network, why do I have to pay for travel, NatGeo, and 100+ channels I never watch?

I have a great idea! I’ll cut cable and sign up for Netflix and maybe Hulu. Genius, saved $100+ per month.

People cut cable to save money, and it worked…for a while.

Everyone unbundled. Competition thrived. Now we have YouTube TV, AppleTV, Netflix, Disney+, Amazon Prime, YouTube Red, Twitch, TikTok, and Paramount+.

The streaming platforms got their distribution, and now they are monetizing, and we pay more than ever: internet plus a stack of subscriptions.

Well, I think we’re at the same place with SaaS. SaaS is at the same place. The cost of building software has fallen to the point where the long tail of applications has become viable for consumers and enterprises. The hardest part of running a software firm has shifted from building to distribution. Network effects and moats are getting disrupted faster. PLG is fueling record, profitable growth to $100M ARR with fewer employees than ever (Lovable hit roughly $100M ARR with about 45 people), but customer churn can be high (Easy to sign up, easy to cancel for a new app). Everyone can have their own version of an application for their phone, the web, or the enterprise.

But Quinn, CFOs have budgetary control; enterprises can build their own software to replace off-the-shelf options. That means LLM spend will go up, but SaaS will suffer.

I agree. Some legacy SaaS and consulting firms will not make the transformation the same way legacy software firms failed to transition their business model to subscription SaaS. But the two forces I see challenging the “SaaSpocolapse” narrative are parity and functional expertise.

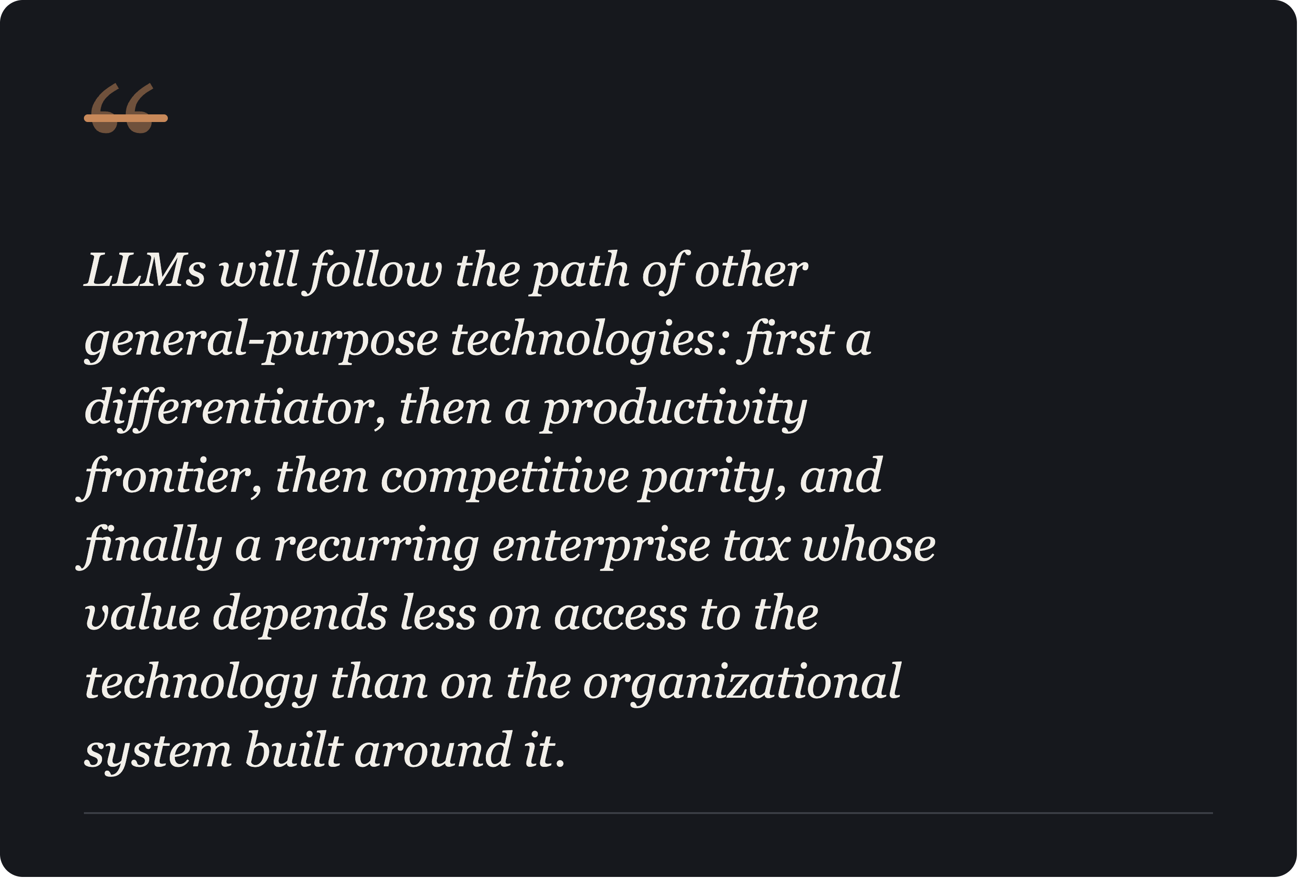

AI software becomes a productivity enhancer and a tax as every firm reaches adoption parity.

Every company will buy the leading SaaS and AI-native offerings, not because they want to, but because they have to. The productivity gains are a forcing function for executive leadership. Speed is the new exhausting moat, and LLMs become both a productivity enhancer and an enterprise tax. The long tail of profitable software means more niche offerings for every problem enterprises, departments, and SMBs face. The counterargument is cognitive load: managing a broad portfolio of apps pushes the dynamic back toward consolidation and bundling. but there is a lot of nuance in that statement, as each department can have its own set of AI software tuned to its exact problems. But that pivot is weaker than it looks, because each department can run its own set of AI software tuned to its exact problems.

Expertise is an accumulation of acquired and applied knowledge.

Retailers, manufacturers, financial institutions, and healthcare firms can build software faster than ever before. If you compare that to the last ten years of SaaS feature releases, you would be right to assume they will benefit from doing just that, building their own software. The assumption we often make when predicting the future is that everything else will remain the same. That is, existing SaaS firms will not take the same technology and accelerate their development and innovation at a multiple or exponential rate over firms whose core business is not developing software.

I do not want to leave you with the impression that enterprises and employees will revert to the old paradigm of outsourcing technical innovation to SaaS firms. Far from it. I believe their innovation will be incremental to existing employee tasks and will incorporate the firm’s proprietary data that is not accessible to third parties. That will force software solutions to be built that solve harder, tertiary problems related to the firm’s core competency. This evolving frontier will continue to drive innovation, churn among SaaS customers, and productivity across the economy.

It is an exciting and exhausting paradigm we are walking into. It’s a version of the “productivity paradox” documented by Nicholas Carr’s 2003 Harvard Business Review essay “IT Doesn’t Matter.”

So the question is not whether software spend goes up. It does. The question is who captures the value creation: the model providers, the AI-native SaaS firms, or the enterprises that turn their own proprietary data into software no vendor can sell them. My bet is on all three, but the majority goes to the firms that execute the right strategy the fastest. And the Net result: everyone will spend more on software, not less, in the years to come.

It’s a good time to sell; it’s a hard time to be in customer success.