The GTM Engineer and the AI Sales Paradox

Why the companies automating everything are hiring the most salespeople, and where one-to-one personalization actually separates B2B winners.

We made it to another Friday, and the whiplash the past week was something else. On one side of the ledger, the frontier kept sprinting: a new class-leading model shipped, three mega-IPOs and mega-rounds soaked up a casual quarter-trillion in capital, and somebody is now building an “artificial general engineer” with enough money to buy a small country. On the other side, the people who sign the checks finally showed up to the party. We talked to a CFO this week who said the quiet part out loud: “We have budgets now.” Four words. They land like a brick.

That is the tension we want to sit in this issue. The frontier goes up and the budget comes down, and everyone selling AI is now stuck in the gap between the two. Here is what is happening in that gap, and who walks away with the margin.

The retention policy nobody read until it mattered

Fable 5 shipped this week, the class model out of the Project Glasswing work, and the bench scores are strong if benchmarks are your thing. But the fine print is doing a lot of work. It is gated for legal, finance, and similar regulated workflows, and a chunk of the security tooling is walled off. The detail that moved customers: the zero data retention carve-out went away, and prompts are now held for 30 days.

For anyone operating models on behalf of customers, that is not a footnote, that is a renegotiation. If you are the operator sending those prompts upstream to the lab, your customer’s zero-retention promise just developed a 30-day hole, and they are the ones who have to explain it to their own security team. We are watching people scramble to sort this out in real time. The lesson that keeps repeating in this market: the model spec is the easy part. The data-handling terms underneath it decide whether the enterprise deal lives or dies.

The cognitive dissonance at the center of the AI economy

The companies whose entire pitch is “we will automate everything” have more open go-to-market roles than any other category. The everything-automation machine needs an army of humans to sell it.

It is easy to call that hypocrisy. We think it is something more interesting. When the cost to build collapses to roughly zero, when everyone can ship the same feature in the same week, the scarce thing is no longer the product. The scarce thing is getting a human to notice, trust, and buy. Distribution becomes the moat. The harness becomes the moat. And distribution, for now, is still made of people picking up the phone.

Look at the role everyone is suddenly hiring for: the GTM engineer. Clay gets the credit for naming it, and the shape of it is a single seller who collapses three old jobs into one. Prospector, closer, and technical pre-sales, all in one person, armed with automations. The promise is leverage: take a rep who used to need a development rep and a solutions architect riding shotgun, and hand them a territory of 1,500-plus accounts they can work.

Two things can be true here. The model is real, and it is not universal. It is a slam dunk when the company sells the exact tool the seller uses to sell. Clay reps prospect with Clay, so they can show a customer precisely how to run the play, and the product feedback loop is tight. That is dogfooding as a sales motion. But you do not spin up a petabyte data cluster to prospect, so the rep selling heavy infrastructure cannot dogfood their own product the same way. The payoff is highest in greenfield, where one person works 50 to 500 accounts and “enrich these 60 logos, find everyone in finance and procurement, draft the outreach, send the invites” is a genuine superpower. In a two-account strategic patch, the same stack is mostly noise. You already know those buyers better than any enrichment tool ever will.

The generalist is back, and the bottleneck has moved

Satya framed a related shift around Microsoft Build: the return of the generalist. We spent a century turning the village blacksmith and baker into assembly-line specialists. AI is swinging the pendulum back. One person now does web dev, hosting, sales, and pre-sales in an afternoon.

We saw it live this week. Take a seven-page proposal, the kind nobody reads because it is all SLAs and compliance boilerplate, and turn it into an interactive site with revenue sliders, so the customer can model their own pricing and watch the numbers populate. Two weeks of designer-and-developer time, done before lunch. Does a slick interactive proposal pull a deal over the line? Maybe not. But every time you lower the customer’s cognitive cost of saying yes, you are winning at the margin, and right now it separates you from the rep still attaching a PDF.

Here is the catch we keep running into, and it is the real story. Building software is become cheap. Shipping is not. The interactive proposal sat finished while we hunted for an internal hosting account and a domain to put it on. The bottleneck is no longer creation. It is the last mile: deployment, permissions, hosting, the boring plumbing that turns a cool artifact into something a customer can open. The teams that win the next 18 months are the ones who solve that last mile internally. Shopify reportedly built exactly this: an internal one-click deployment surface where any employee can drop in an AI-built app or demo, and it publishes, securely, behind the company walls. That internal deploy button is quietly one of the highest-leverage things a company can build right now.

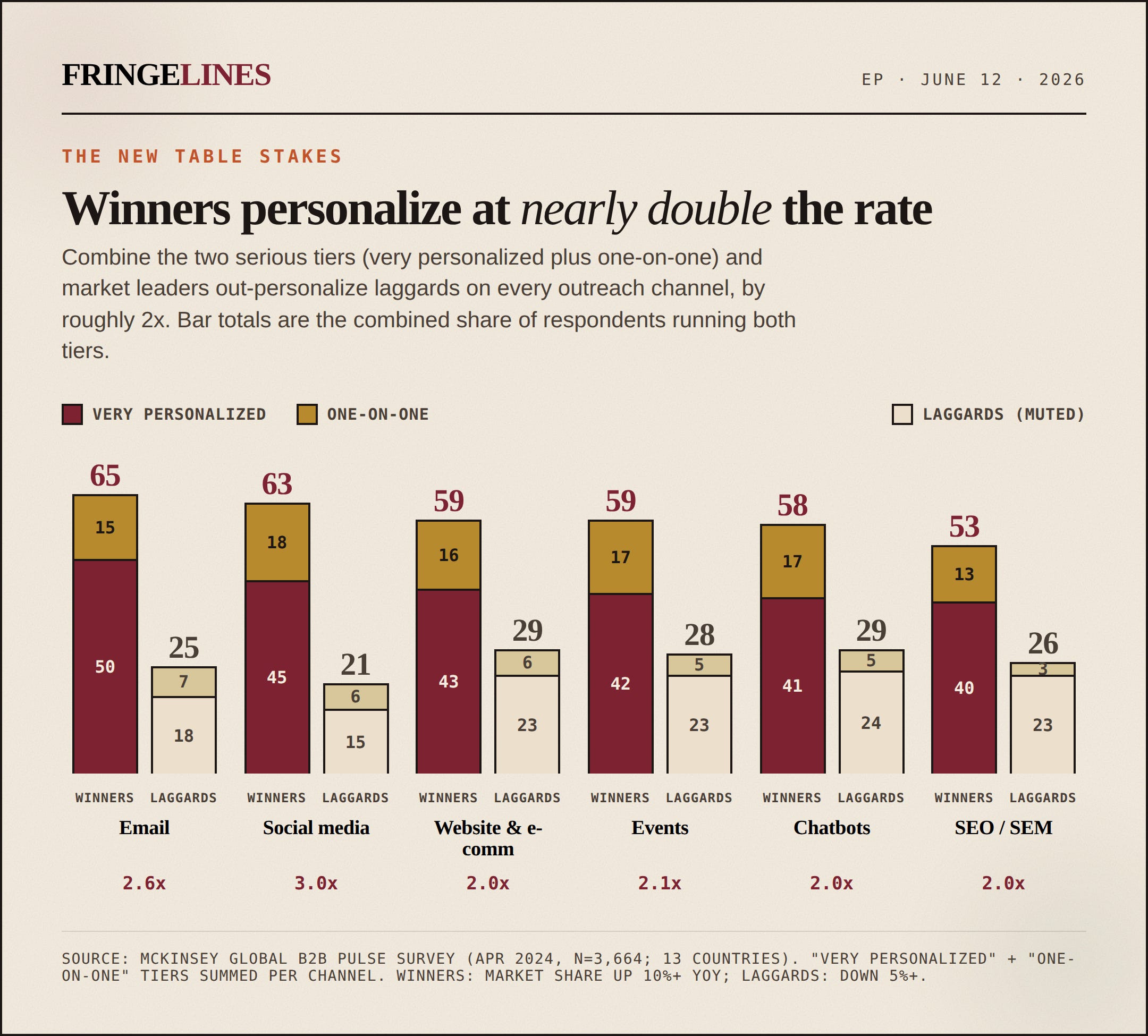

Personalization at scale is the new table stakes, and the floor keeps rising

McKinsey’s latest B2B Pulse surveyed roughly 4,000 decision-makers across 13 countries, and the headline is blunt. Omnichannel, e-commerce, digital tools: all table stakes now, none of them a differentiator. What separates leaders from laggards is one-to-one personalization, real generative-AI use, and tight account-based-marketing governance as a control layer.

The number that matters: market leaders are about 4 times more likely than laggards to run true one-to-one personalization, 20 percent versus 5 percent. Personalization used to be the swap-in variable fields in Salesforce, and it never scaled past that. AI is the first thing that lets you do individual outreach across a real account list without the economics falling apart.

But scale cuts both ways. The same engine that personalizes 500 messages can scale a single mistake to 500 inboxes. Wrong product, wrong price, a typo that references the wrong company, now shipped at volume. The auditing layer is not optional; it is the whole job. This is why “send one more message” no longer fixes anything. When everyone can generate infinite outreach, volume is noise. The differentiator is knowing something true about the buyer and adding a human touch on top. Which loops right back to the GTM engineer: this entire motion is predicated on pulling first-party, second-party, and third-party signals into one enriched view, and most teams still cannot connect those pipes.

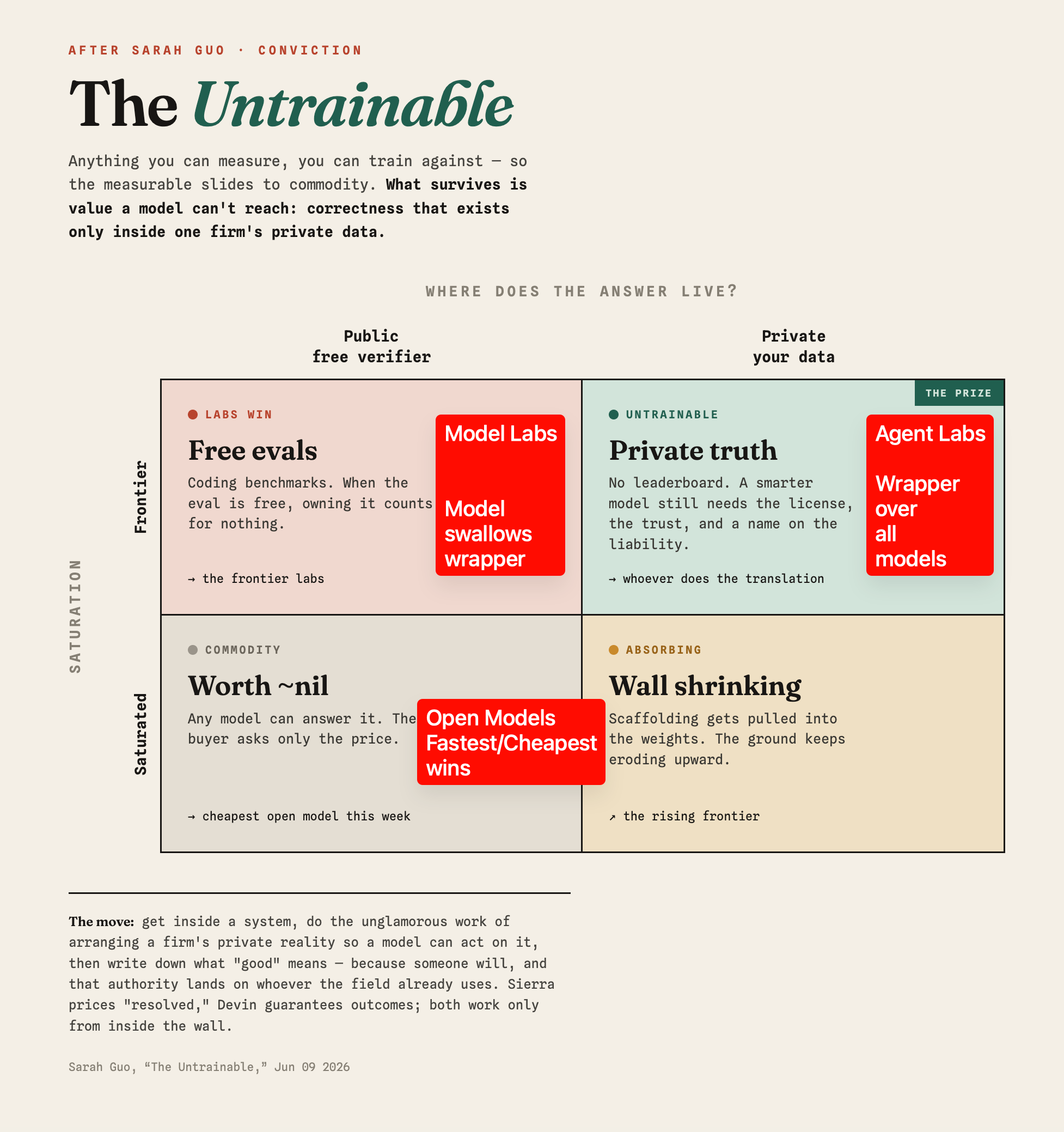

The 2x2 that explains who keeps the margin

The cleanest mental model we found this week is a 2x2, the framing traces to Sarah Guo. The best line in it: what you can measure, you can train against, and anything measurable slides toward commodity. What survives is the value a model cannot reach, the correctness that exists only inside one firm’s private data.

Lay it out. One axis is task difficulty, saturated versus frontier. The other is the data, public and freely verifiable, versus private with no public leaderboard.

Frontier plus public data: the labs win, every time. Coding benchmarks live here. The best model takes it.

Saturated plus public data: pure commodity. “Summarize this email.” Cheapest, fastest model wins, and the value rounds to zero.

Saturated plus private data: the wrappers. Harnesses around a model, living on proprietary data that the labs cannot see. This is the contested middle, because the labs are marching straight into it, absorbing legal, finance, and security, while the wrappers race to stay ahead on domain data that the labs still do not have.

Frontier plus private data: the promised land. Your company’s data, or the pooled data of all your customers, at a scale no one else can touch, combined with frontier capability. Nobody can commodity-price you out of this corner.

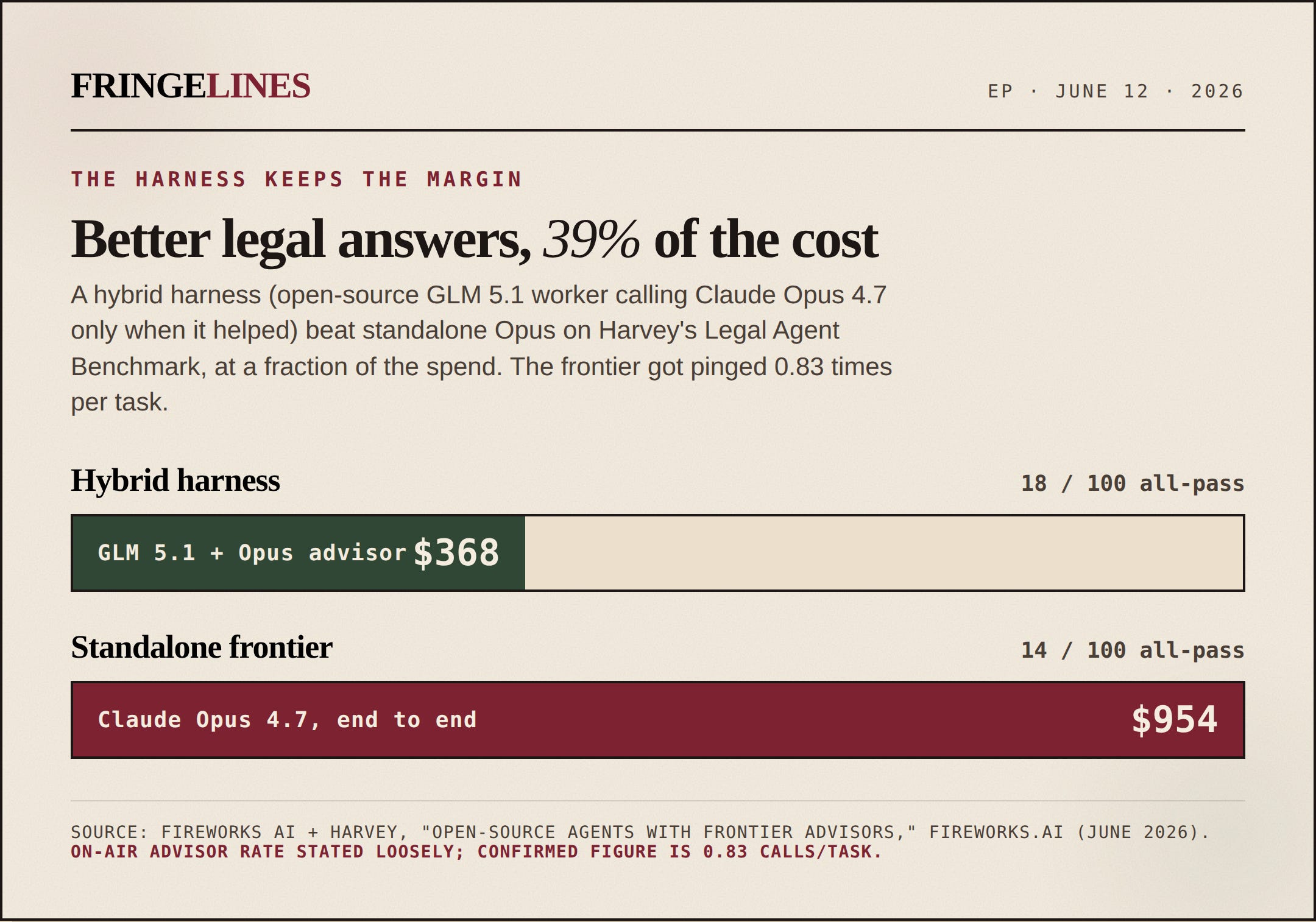

Now the part that pays. Harvey and Fireworks published a legal-AI result that makes the margin story concrete. A hybrid harness with an open-source GLM 5.1 worker, calling Claude Opus 4.7 as an advisor only when it helped, hit 18 of 100 full-rubric passes at 368 dollars total. Standalone Opus scored 14 of 100 at 954 dollars. Better quality, roughly 39 percent of the cost, and the worker pinged the frontier model just 0.83 times per task on average.

The outcome is not the point. The margin is the point. If the lab attacks a legal task directly, it charges the customer and keeps the spread. If the wrapper performs the same task at a fraction of the inference cost through smart routing, it can price below the lab, still save the customer money, and pocket the difference. That is how AI application gross margins climbed from the low 40s to the high 50s, even as raw inference costs rose. The harness captures the value the model leaves on the table.

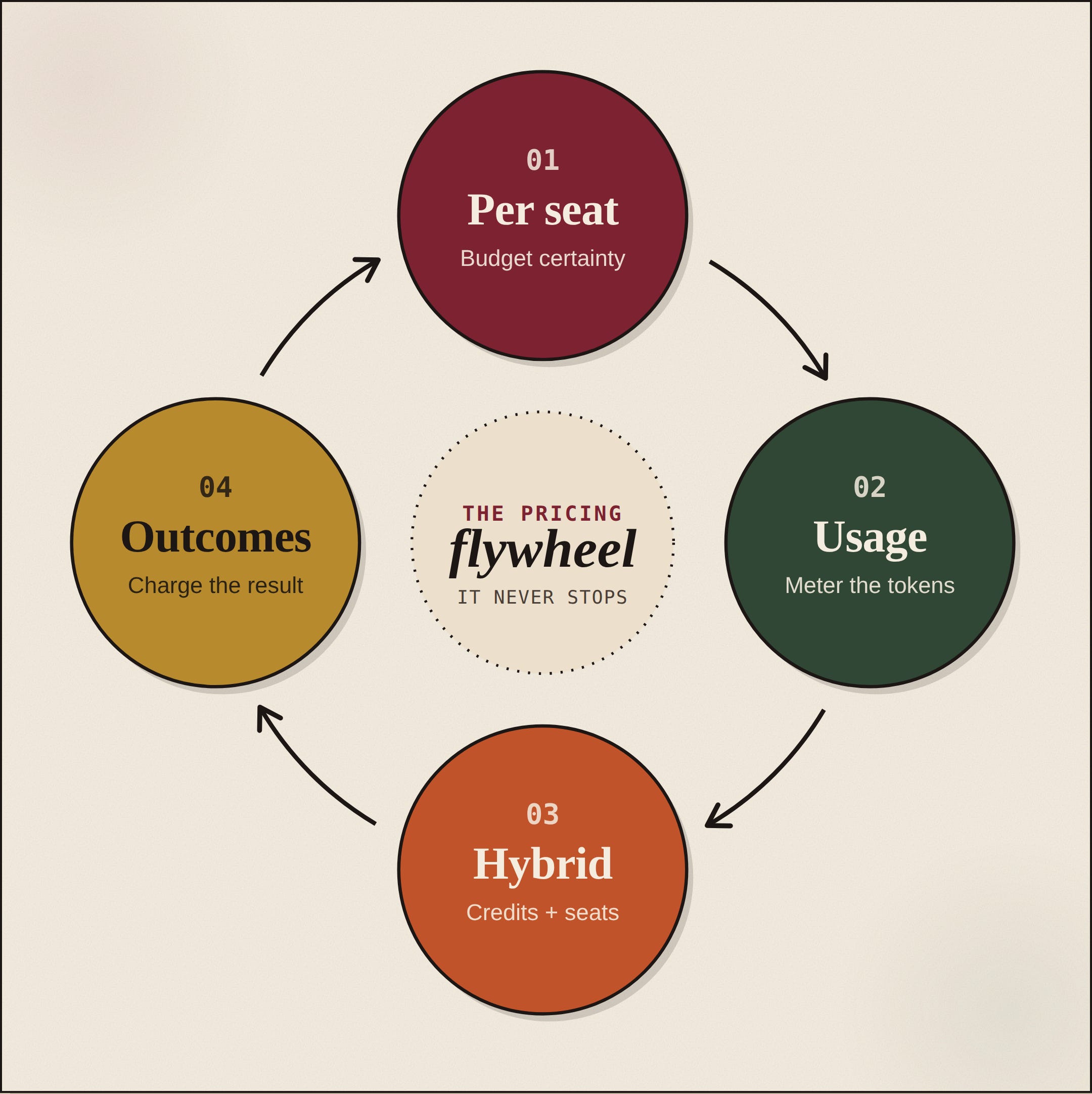

The pricing wheel never stops turning

We will leave you on pricing, because it ties the whole issue together. The durable take, echoing comments from Satya Nadella: per-user pricing is an artifact of buyers needing budget certainty, and it survives even as consumption metering slides underneath it. Subscriptions bundle usage into per-seat stacks, with consumption below; that is the adjustment GitHub Copilot made after real usage blew past what a flat seat assumed.

Watch the cycle. 1/ Per-seat could not hold once intensity exploded, so vendors moved to 2/ usage. Usage, credits, and seats became the 3/ hybrid. Next comes 4/ outcome pricing: charging for the result rather than the tokens. And the moment outcomes get predictable, buyers will want their margin back, ask for a discount, and push the whole thing back toward fixed budgets and seats. Then we’re back to per-seat pricing.

It is a wheel, not a ladder. That sounds exhausting, and it is, but it is also the most bullish thing in this issue. Humans are never satisfied. The second a cost becomes predictable, we want it cheaper, and we invent something new to want. Somebody has to go figure out what we want next and build it. That churn is the job. As long as it keeps turning, there is work in the gap between the frontier and the budget.

So: the frontier goes up, the budget comes down, and the whole game is who captures the value in the middle. Our bet stays the same. Build relentlessly, but spend at least as much energy on distribution and the last mile, because that is where the margin lives. Just go build. Then go figure out how to get it in front of someone.

See you next week.

Fringe Lines covers the business layer of the AI industry for builders and GTM operators. Forwarded this? Subscribe at newsletter.fringelines.io.