What happens to you when the AI Bill Comes Due

The week tokenmaxxing peaked, $100M CRO packages went parabolic, and the hyperscaler that quietly figured out the economics pulled ahead

Last week was a slow week, on paper. Short holiday cycle, almost half the calendar gone, kids home from school (bye bye productivity). And yet, on this sleepy holiday week, OnlyCFO shared a hypothesis: AI spend is now the largest vendor line item on many P&Ls. Mind-bending growth in 2026 is moving so fast it’s breaking the status quo, budgets, and pendulum swings.

Here is our read on the topic that caught our eye this week across Sales compensation, usage vs. contract bookings, and Tokenmaxxing. But first, the headlines…

Fringe Lines is a reader-supported read on AI, builder tooling, and go-to-market. If a friend forwarded this, subscribe.

1. The comp bubble at the top, and what it tells you about the sustainability of AI-first companies

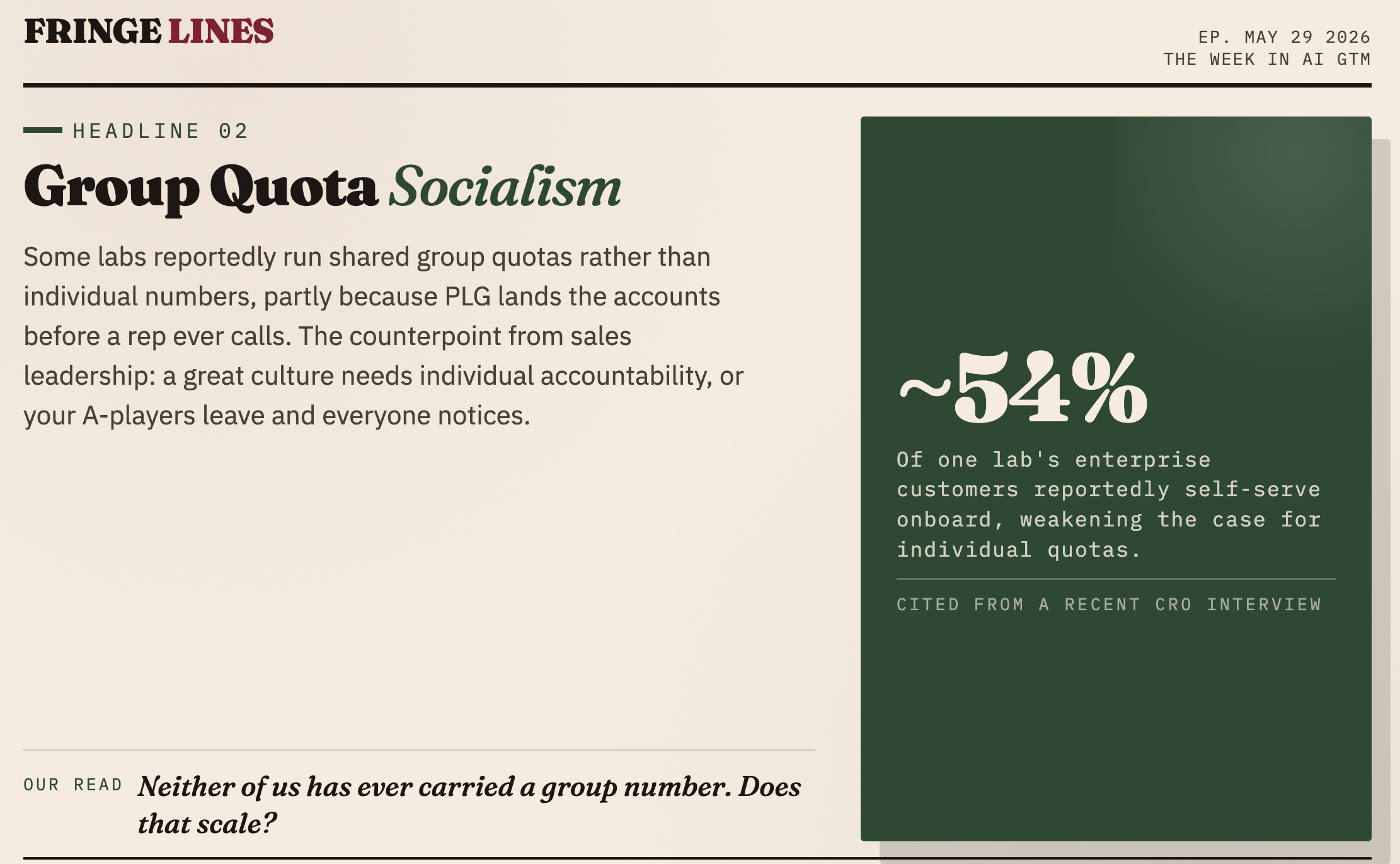

Start with the number that broke our brains this week. Top-tier CROs AI startups are reportedly fielding packages up to $100 million. Bubble anyone? The entire premise of the AI sales era is that the motion is automating itself: AI SDRs, automated lead enrichment, self-serve onboarding, doing the work a body used to do. So why is the person at the top of that org worth nine figures?

The answer is the tension we kept circling back to. We heard this week that a lot of these AI companies in exponential growth are running group quotas, not individual ones. No personal number. There are decent arguments for group quotas. How do you set quotas for once-in-a-generation growth percentages? I can tell you, finance doesn’t want to pay the accelerators, so they default to equity. If the company wins, you’ll overachieve in the IPO.

That works right up until it doesn’t. Our concern, and we are not alone here, is the sales-socialism challenge. If nobody carries an individual number, you slowly accumulate quiet underperformers who have never had to win a deal on instinct. A real sales culture culls the bottom 10% on a rolling basis based on performance, so that overachievement, president’s club, and grinding mean something. Strip out accountability, and the whole thing looks great while demand is a tailwind, but the faster revenue and production adoption ramps, the faster it can drop if you don’t have strong moats to maximize switching costs (network effects, distribution, scale economics).

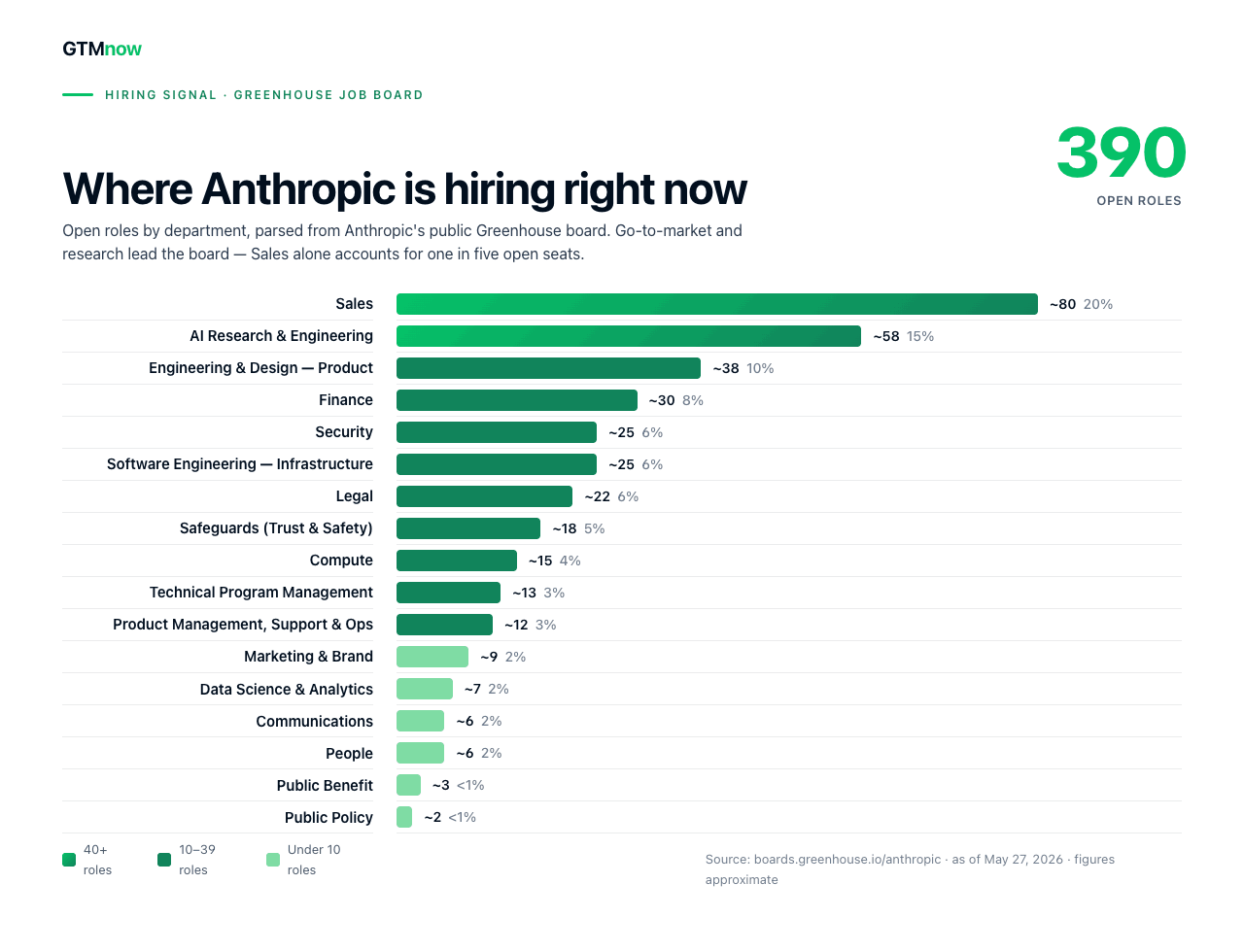

Compensation aside, one if the interesting takeaways from 2026 is counterintuitive, but an optimistic one. AI will not replace the rep. The flood of AI-generated outbound made cold digital noise nearly worthless, which raised the premium on the human who makes the phone call, leaves the voice mail, sends the text, and shows up in the room. Human interaction is the differentiator, and you can see this in the percentage of sales job openings among total openings at the fastest-growing AI companies.

Chart courtesy of GTMnow.

2. Contracts are friction. They are also the only thing stopping a one-click exit.

The comp story rests on a deeper one about contracts, and this is where it gets uncomfortable for fast-growing AI PLG companies that prioritize growth over commitments. Inserting commitments and contracts into your sales cycle adds friction on the front end, elongating the sales cycle and therefore slowing growth. It also acts as friction on the backend, helping reduce churn. You need a balance of commitments with Account Teams, also held responsible for usage. Otherwise, you risk shelfware or commitment shortfalls that churn because the economics are so bad.

The former CRO who took Snowflake from zero to $4 billion framed it cleanly: contracts act as friction against churn. They buy you time. A customer under contract cannot quietly decide on a Tuesday to migrate off and never speak to you again. They have to come to the table, just as a data center lease forces a conversation. Month-to-month is more expensive precisely because optionality has a price.

Now layer in what we heard recently at SaaStr’s conference, more than half of Anthropic’s enterprise customers are self-serve onboarding. I believe they did this out of necessity, can’t scale hiring and onboarding fast enough, and because they weren’t willing to lower their bar for talent. The challenge is that Anthropic has OpenAI chasing after more Enterprise use cases with its Codex offering, desktop app, and availability on Amazon Bedrock. If half your enterprise base is not talking to a rep, then half of it is almost certainly not signing anything either. Which means the thing that used to protect you on the way down has been deliberately removed in the name of frictionless growth on the way up.

Founders will tell you that contracts add friction to the acquisition process, and they are right. It is a genuine double-edged sword: it helps you climb, and it hurts you when you fall. But the version of this that should worry an AI seller is the customer who says, “We love your models. We put OpenRouter in front of everything, pay a small premium, and cut our costs by 40% by routing the easy work to cheaper models. Just keep making great models, we will consume them our way.” What is your rep supposed to say to that? “Do you have a contract?” “No, we’re good.”

There are options for the Labs. You can gate your newest models. You can stop subsidizing third-party harnesses, which is exactly why Anthropic pulled third-party harness access off its most subsidized consumer plan: why pay to drive adoption of someone else’s wrapper. The harness is becoming a real moat. But every one of those answers points in the same direction. The percentage of enterprise customers you actually talk to has to go up from 50% as you scale your Enterprise Sales team. The other challenge with commitments, customers expect discounts in exchange for the lock-in of usage. That is another challenge for Labs as they strive for profitability ahead of an IPO. A 5% discount doesn’t sound like much unless your EBITDA is 5% as well.

3. Tokenmaxxing met the finance department in 2026, and your CFO is not impressed

AI optimism above runs straight into a wall of worry this week, the AI bill is coming due.

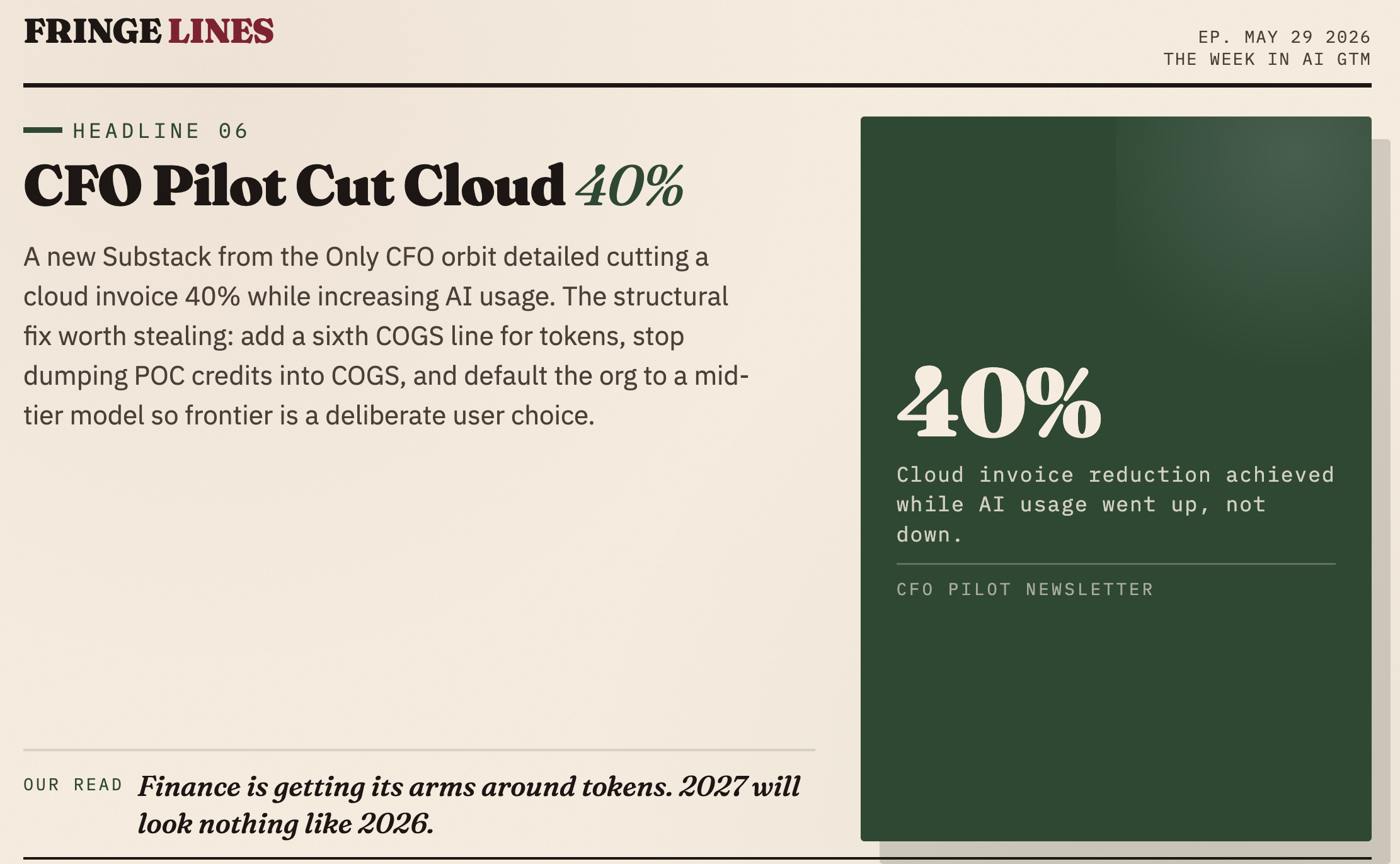

A stat to carry into Monday, courtesy of CFO Pilot citing Ramp’s spend data, is that the average business is now spending 13x more on AI tokens than it did in January 2025. Less than eighteen months, basically zero to the largest vendor line on the sheet. Uber’s COO publicly said the company burned through its entire 2026 AI budget in four months and that the link to shipped consumer features “is not there yet.” Amazon reportedly scrapped an internal AI usage leaderboard, with leadership telling staff not to use AI just for its own sake. Microsoft reportedly canceled Claude Code subscriptions for several product divisions. Fortune declared the era of measuring AI value by tokens consumed officially over.

This is Goodhart’s law playing out in real time. When a metric becomes the target, it stops being a good metric. Hand an org a token leaderboard, and people will run it just to run it. The fix is not spending less; it is spending like an adult. CFO Pilot’s line is the keeper: “You don’t use a heart surgeon to take your temperature.” A $100K-per-month Opus bill drops by roughly 48%, which is $576K of savings on an original 1.2M run rate, by routing easy work to cheaper model tiers. Set the org default model to the middle tier, and 90% of users just stay there, which is up to 40% in savings before you do anything clever. Add per-user spend caps, prompt caching for repeated contexts at roughly 90% off the cached portion, and the Batch API at 50% off for anything that does not need to happen in real time.

Finance is getting its arms around tokenmaxxing in 2026. 2027 is going to look very different.

4. How the Hyperscaler Capex gives insight into differentiation

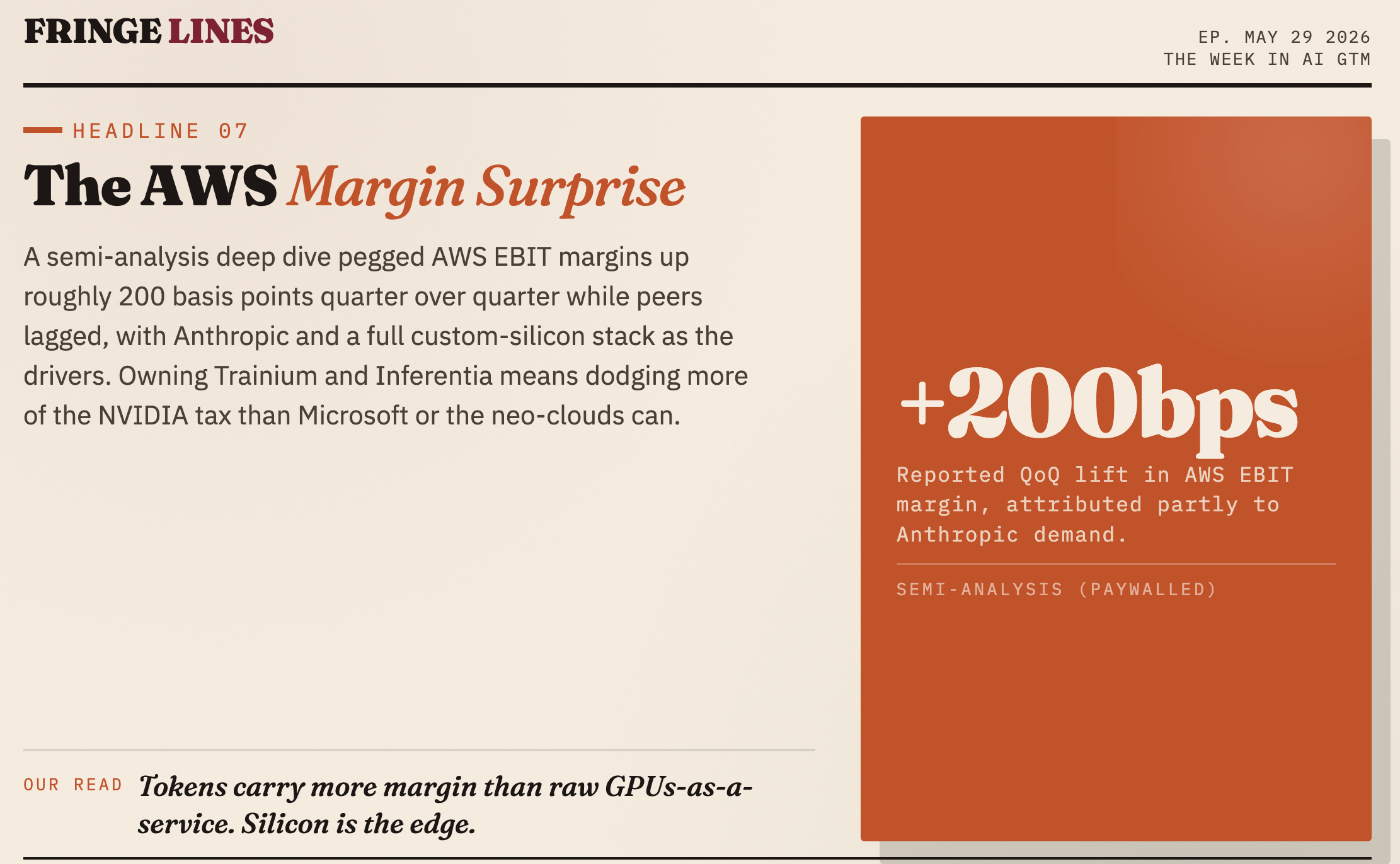

The framing that lit us up this week, via SemiAnalysis, is who actually makes money on the economics of tokens. The first tenet: tokens carry more profit for a hyperscaler than raw infrastructure-as-a-service, because if you are just renting GPUs, you are largely subsidizing the chip vendor. Tokens-as-a-service is a fundamentally better business model than the IaaS contract it sits atop.

Then it becomes a question of whose silicon is being used in each cloud. Amazon has Graviton for general compute and Trainium for training and inference, and a large share of its managed inference reportedly runs on Trainium, which means it is dodging a chunk of the NVIDIA tax. Google has TPUs doing a similar job. Microsoft is still largely NVIDIA, AMD, and Intel while it builds its own. The Neoclouds, CoreWeave, and Oracle tiers are essentially NVIDIA resellers. Advantage: the two players who built their own silicon.

Now let’s pivot to capacity to handle customer GenAI workloads, which includes energy, data centers, compute, and silicon. Amazon and Google moved first to lock in energy commitments, so they had the capacity to open data centers when demand showed up.

Next, let’s look at how each company is meeting their customer demand for capacity (Internal and external).) Microsoft has to host its own Copilot, GitHub Copilot, and OpenAI inference. Google has to power its own search, its Frontier training, its Gemini Workspace assistant, and Claude models on top of GCP. Amazon, by comparison, has more of its built capacity free to sell, and in a world where demand still outruns supply, that surplus converts straight into margin. Net: AWS operating margins expanded meaningfully quarter over quarter, while peers went flat to down. Hypothesis? Amazon’s vertically integrated stack, combined with Amazon Bedrock's hosted model revenue charged to end customers rather than internal business units, is driving token profitability.

We cannot independently verify the full profitability ranking, and the most interesting numbers here are extrapolations rather than disclosed figures, so take them with a grain of salt. But the strategic shape is sound, and it reframes the buying conversation. It is not just “Claude or OpenAI.” It is “which cloud are you buying through, and what does that do to your effective unit economics?” Most buyers are not asking that question yet. They should be. Check out SemiAnalysis’s article for a deep dive into the token economics.

Where this leaves us

The thread connecting all of this week’s topics is a pendulum. We are at peak GenAI hype (tokenmaxxing) on the Gartner hype curve, the part where horizontal AI will eat all Software and jobs globally, and we think the swing back toward reality is starting. That is healthy and refreshing. The cortisol of the past six months is starting to take its toll. The reason both major labs entered into joint ventures with consulting firms is that GenAI/LLM adoption and ROI are genuinely hard. You do not peanut-butter-smear AI tokens onto a problem and magically get your ideal outcome.

The analogy we ( read everyone) keep coming back to is electricity. If large language models are the general-purpose technology, the raw current, then what we are still missing is the appliances, the specific products that convert that current into productivity. Right now, we are at the light-bulb stage: personal output per person is up, but companies have not figured out how to capture that gain at the team, function, or firm level. The honest possibility is that there is a real ROI already here and simply not surfacing, because the person who saved two hours drafting feedback with Claude is reinvesting that into their next AI project or taking a longer lunch. People could be quietly getting more done and not giving the time back to the employer. I think a more nuanced and balanced attestation is that more people can do more tasks outside their core domain or skill set. This won’t immediately lead to a productivity boon, but as employees skill up on a broader set of tasks, the productivity will trickle through the firms.

If we are right, the revenue curve flattens as customers optimize their spend, then turns back up sharply once verifiable ROI becomes clear and the rush to scale use cases with provable ROI begins. The open question, the one that decides the winners, is whether the labs can become cash-flow positive fast enough to still be standing when that second wave arrives. With the amount of capital being pulled out of the market this year from the IPOs, it’s an open question.

Come back for more sauciness next week.

Fringe Lines is a reader-supported read on AI, builder tooling, and go-to-market. If a friend forwarded this, subscribe.